by Numera | Apr 2, 2025 | Bookkeeping and Accounting, Business Management

Bookkeeper vs accountant: when it comes to managing your business finances, the terms bookkeeper and accountant are often used interchangeably. However, they perform very different roles. Understanding the difference between accounting and bookkeeping is crucial for business owners who want to stay compliant, make informed decisions, and plan for sustainable growth.

At Numera, we help Brisbane-based businesses take control of their finances through expert bookkeeping support. In this article, we’ll break down the key differences between bookkeepers and accountants, explain what a bookkeeper does, and help you decide which professional is right for your business.

What Is a Bookkeeper?

A bookkeeper is responsible for recording and organising your day-to-day financial transactions. They keep your business’s financial records accurate and up to date, which is essential for tracking cash flow, managing expenses, and preparing for tax time.

Typical Bookkeeping Tasks Include:

Bookkeepers are hands-on with the numbers, working closely with business owners to ensure everything runs smoothly behind the scenes.

What Is an Accountant?

An accountant uses the financial data prepared by a bookkeeper to provide higher-level financial analysis and strategic advice. Accountants help businesses interpret their numbers, ensure compliance with tax laws, and make informed decisions for long-term success.

Key Accounting Responsibilities Include:

-

Preparing and lodging tax returns

-

Providing financial and business advice

-

Developing budgets and forecasts

-

Managing company structure and compliance

-

Conducting audits

-

Analysing profitability and performance

While accountants can provide bookkeeping services, they typically focus on the bigger financial picture.

Bookkeeper vs Accountant: Key Differences

So, what is the real difference between accounting and bookkeeping? In simple terms:

Bookkeepers are essential for maintaining accurate records and staying on top of day-to-day tasks, while accountants are more involved in compliance, reporting, and strategic planning.

Do You Need a Bookkeeper, an Accountant – or Both?

Most small to medium-sized businesses in Brisbane can benefit from working with both a bookkeeper and an accountant. A bookkeeper ensures your financial data is accurate and timely, making it easier for your accountant to provide valuable insights and support.

At Numera, our qualified bookkeepers collaborate with your accountant to ensure your books are in excellent shape and your business stays on the right track.

Why Bookkeeping Is Essential for Your Business

Accurate bookkeeping isn’t just about compliance – it gives you clarity and confidence in your business decisions. Here’s why smart Brisbane business owners choose professional bookkeeping:

-

Stay organised: Avoid the stress of missing receipts or scrambling at tax time

-

Save time: Focus on running your business, not balancing the books

-

Improve cash flow: Track what’s coming in and going out in real time

-

Support growth: Make informed decisions with accurate financial reports

-

Ensure compliance: Stay on top of ATO deadlines and reporting requirements

Choose Numera: Your Brisbane Bookkeeping Experts

If you’re wondering whether you need a bookkeeper or accountant, start by making sure your books are in order. At Numera, we provide reliable, efficient, and professional bookkeeping services tailored to Brisbane businesses.

We’re more than just number crunchers – we’re your financial support team. Whether you’re a start-up, sole trader or growing business, we’ll keep your finances clear, compliant, and under control.

FAQs

What is a bookkeeper?

A bookkeeper is a financial professional who records and manages your business’s daily financial transactions. They help keep your financial records accurate, up to date, and compliant with ATO requirements.

What is the difference between accounting and bookkeeping?

Bookkeeping involves recording and organising financial data, while accounting involves interpreting that data to provide strategic financial advice, prepare tax returns, and support business planning.

Should I hire a bookkeeper or an accountant?

Both professionals play important roles. If you need help managing your day-to-day finances, a bookkeeper is essential. For tax planning and financial advice, you’ll want to work with an accountant as well.

At Numera Bookkeeping Services, we provide more than most traditional bookkeepers. With significant experience across a wide range of industry sectors, we are able to support you with all the standard bookkeeping services as well as BAS preparation and lodgment, payroll outsourcing services, advice on the selection of accounting packages and software training. If you need the services of a local accountant, our referral partners, MGI South Queensland are on hand to offer more detailed accounting advice. Work with the Brisbane bookkeepers you can trust. Give us a call today on 07 3002 4880 or email info@numera.com.au to find out how we can help your business.

by Numera | Oct 7, 2023 | Business Management

by gpm | Mar 2, 2021 | Business Management

“I can’t work any harder and I don’t know how my business is travelling.”

“I don’t feel like I understand my business.”

“I made $300k last year, was it a good year?”

“Numbers give me headaches”.

“My accountant tells me I have to $50k in tax as I made a profit last year. But WHERE IS THE CASH?”

These are some of the most common refrains we hear from clients. These are all heart-felt cries for help for no-nonsense, simple ways to understand their businesses, how it operates, its financial performance and its ability to provide for a lifestyle.

How To Run Your Business More Efficiently

After having worked with numerous businesses from many industries, we found that the following process works the best in helping our clients:

- Having regular meetings with them to help to spend time working on their business, not just in it;

- Providing them with easy-to-understand and yet at the same time, sophisticated reporting on the key metrics for the business; and

- Providing them with a sounding board to make decisions.

The centrepiece in our process is our ability to provide easy-to-understand reports focusing on the key metrics for the business. These provide our clients with the “hard numbers” from which they can come up with options and make decisions.

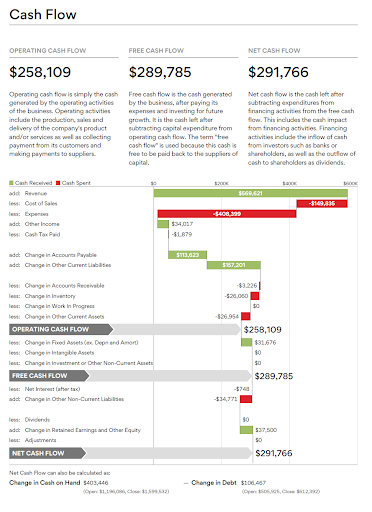

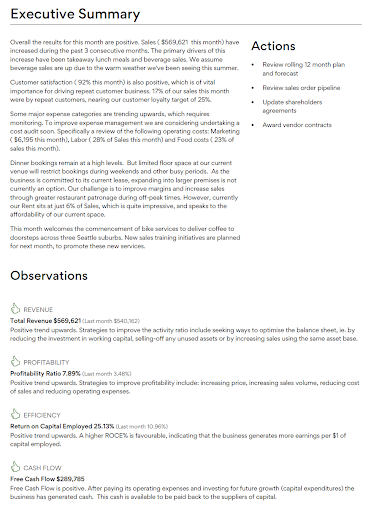

For example, it is no secret that the hospitality industry has had a tough time lately due to the lockdowns. It is now even more critical for the owners of restaurants and cafes to keep a close eye on their numbers. Here are some of the screenshots from reports prepared for a restaurant client. Accounting and Management reports like these have proven to be extremely helpful in helping the client in making the right decisions to thrive and not just survive in the current downtown.

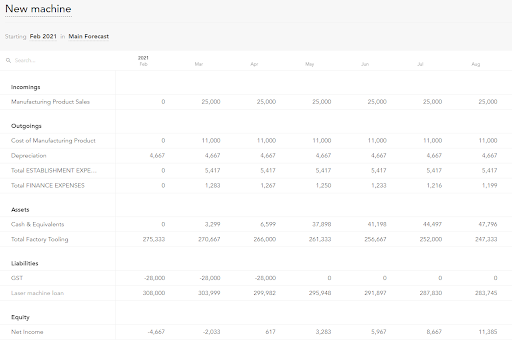

Here is another example from a what-if analysis we did for manufacturing client, whose business received a bump in sales as they supplied products which were in high demand due to the lockdowns. In this case, they asked us if they can afford to invest in a particular piece of machinery to keep up with the increased demand, and we were able to answer their question on the spot with an instant profit and cash forecast which our purpose-built software is capable of.

Numera have helped many businesses to increase their profitability and manage their businesses more efficiently. If you would like to talk to one of our senior team about how we can help you understand and grow your business and improve its profitability, give us a call on 07 3002 4800 today or fill in your details below and one of the team will be in touch.

by gpm | Mar 2, 2021 | Business Management

Shrinkage in the retail sector has a major impact on the profitability of supermarkets and other stores. Shrinkage is the result of theft by customers and staff, and is also caused by damage to goods as a result of poor ordering and handling practices. It can be equal to three per cent of sales at some independent supermarkets. The shrinkage problem tends to be worse in smaller stores with an average shrinkage factor of around five percent. If retailers want to improve profitability they first need to understand shrinkage.

A recent case study revealed a supermarket business turning over 10 million dollars per year while poor shrinkage control contributed to losses of 10 thousand dollars per week off its bottom line. It seems the smaller a supermarket is, the higher the shrinkage problem. As independent supermarkets increase their turnover, the shrinkage problem reduces to an average of around 1.75 percent. Better quality systems, and better management of the factors that drive shrinkage, contribute to the lower figure in larger supermarkets. Best practice operations are achieving shrinkage levels of less that 0.5 percent.

In reality, most supermarket operators do not know the true cost of shrinkage. Often this is the difference between success and failure of the business particularly when profit margins are so tight. An improvement in shrinkage management of just one per cent of sales can improve profitability by thirty-three percent. This type of saving can enable retailers to channel their resources into areas which will make a positive impact upon their cash flow.

Identifying Shrinkage

Shrinkage can be defined as the loss in margin due to poor stock management procedures, reporting practices and internal controls. It is measured by comparing the gross margin from the Point of Sale (POS) Report to the financial accounts or internal stock management reports.

Some of the factors that contribute to shrinkage include theft by customers and staff in the supermarket, inconsistent pricing practices, excessive and uncontrolled discounting, absence or infrequent stock taking, as well as damage to goods as a result of poor handling and ordering practices. For managers and owners, shrinkage is a very attractive area to address as the benefits flow straight to the bottom line. We advocate benchmarking the store to identify the gravity of the issue.

Some of the best practice operators have achieved low shrinkage levels by implementing stock management systems, which are compatible to existing POS systems, allowing for automatic re-ordering, regular rolling stock-takes on high-risk items, and stock management procedures. These systems are supported by staff training and job descriptions and assigning responsibility to selected staff, thus delivering tangible benefits to the supermarket owner.

Just some of these benefits include improved cash flow from reduced stock levels, as a result of ordering of stock consistent with sales demand, reduced theft by making high risk items more visible to staff, and providing an early detection of pilferage through instant stock management reporting.

This type of improvement enables the retailer to then direct their resources into other areas, such as improving their supermarket layout and design. Shrinkage efficient supermarkets are most likely to survive and thrive in a competitive market. To improve profitability allows retailers access to funding for supermarket refurbishments, which is an essential part of competing for market share against national chains.

Shrinkage Reduction Planning

Financial benefits show as soon as a supermarket addresses its shrinkage problem. The best way to begin this process is for the retailer to talk to a professional adviser, or seek advice from industry specialists to develop an action plan to implement better operational practices.

Most retailers are time-poor and work long hours so the most effective way to develop a shrinkage plan is to identify your immediate goals, determine what resources are required (money, people, and time) and allocate tasks to responsible persons. One of the biggest shrinkage issues is that supermarket owners do not compare their management account gross profit (GP) percentage with what comes out from their POS system. This is a big mistake. We found most retailers were unable to produce accurate management accounts on a timely basis and most often conduct stock-takes once a year for tax purposes.

Shrinkage loss really hits home when retailers compare their GP in the financial accounts provided by their Accountant to POS reports. The key is to develop a stock management system that allows for timely and accurate management reporting. Our industry manager recently saw supermarket figures showing a nine percent difference between the POS GP percentage and accounting GP percentage.

For example, regular weekly stock-takes of high wastage and theft items (e.g. meat and fruit/vegetables and tobacco) and cyclic stock-takes on other items will allow for effective monitoring of GP variances.

Adopting a standardised chart of account and journals will improve management reporting of shrinkage as scanning systems ignore the issue. Some supermarket chains have front-end systems that record all customer returns and place the reason for the return and reports at the back office each day and for the week. Further ‘reduced to clear items’ are also all managed via the front end.

Some chains also ensure its cleaners to place floor waste into a separate bin. This separate bin is then checked to see what products the cleaners have swept up and if these products can be reclaimed. It is important that staff take the time to monitor stock, even if it does mean checking the dairy fridge more frequently. You can use technology to keep track of perishables within the supermarket.

If you’re struggling to get clarity on your gross profit margins and want to improve profitability, talk to the team at Numera about our Virtual CFO and Accounting Reporting services.

Disclaimer: this information is of a general nature and should not be viewed as representing financial advice. Users of this information are encouraged to seek further advice if they are unclear as to the meaning of anything contained in this article. Numera accepts no responsibility for any loss suffered as a result of any party using or relying on this article.

by Numera | Nov 13, 2019 | Bookkeeping and Accounting, Financial Literacy

When you’re running a small business, engaging the right support to help you fulfil your tax obligations and keep your business in good shape is vital. But the terminology used can sometimes be confusing. Quite often you’ll hear the phrases: tax agent, BAS agent and accountant used interchangeably but the perception that they all do the same thing is wrong. There are important differences between the roles and it’s important to understand them so that you get the right support. So what is a BAS agent and what is the role of a tax agent and accountant and how do they differ?

What Is A BAS Agent?

So let’s start with a BAS agent. As we highlighted in a recent blog, BAS Requirements For Small Business, it stands for Business Activity Statement and it is used to report on and pay several different types of taxes including Goods and Services Tax (GST) and Pay As You Go (PAYG) instalments. A BAS agent is therefore authorised to prepare and lodge a BAS return on a business’ behalf and provide advice on your day to day business taxes, primarily limited to your GST and PAYG obligations.

Regulation for BAS agents was introduced in 2010 to ensure that contract bookkeepers, who had traditionally assisted small business owners with their GST and PAYG, were appropriately qualified to offer this support. Following the amendment of the Tax Agent Services Act, to become a Registered BAS Agent you need to have 1000 hours of experience in providing these services, have professional indemnity insurance and pass the ‘fit and proper person’ test. This set in place a distinction between the role of a bookkeeper who may be doing data entry and bank reconciliations for example and someone qualified to prepare your BAS statement. Many bookkeepers had to complete or update their knowledge, primarily around GST legislation, to continue offering this service.

While this isn’t quite as detailed as the requirements for a Registered Tax Agent, it means that those completing your BAS have a level of experience specific to these needs and are legally accountable to the Tax Practitioners Board. A good BAS agent can prove invaluable to your business as they can make it so much easier for your accountant to offer sound advice based on an accurate picture of your business financials.

What Is A Tax Agent?

The role of a tax agent is a little different to this. Tax agents are more specialised and qualified in tax law. Providing they are registered with the Tax Practitioners Board they are licensed to prepare and advise on a broader range of tax issues including but not limited to an income tax return and they are suited to working with growing businesses. When it comes to doing your business taxes, they will review all your annual income and expenses and ensure that you get all the relevant tax deductions available to you. Keeping your business tax liability at a reasonable level is critical when you’re running a small business. A good tax agent is therefore essential as they take away the pressure of needing to understand the ins and outs of your tax liability, what you can claim as expenses and deductions and what you can’t.

So how do these roles differ from that of an accountant?

What Is The Role Of An Accountant?

An accountant is the heavyweight when it comes to managing and growing your business. A good accountant will perform a number of critical roles for a business including (but not limited to) ensuring that you are operating under the right business structure, helping you with strategic planning, financial management, tax planning, wealth and risk management. A good accountant will be your trusted business advisor, keeping you on track and explaining the implications of your key business decisions to maximise for business and financial success.

So whereas a BAS agent and a tax agent are both involved in dealing with lodgment and compliance, the role of the accountant is to help you take a longer-term view of your business and to help set you up to achieve your business goals. While an accountant should effectively be able to perform both of the above roles, their level of expertise to advise on a much broader range of issues means that their hourly rate is typically higher. This means you are better off engaging the right professional for the right job. Each professional performs a unique but important role, depending on the needs of your business and working with all of them at the right time ensures you are covered in terms of both compliance and business growth.

And what if you can find a bookkeeper who is also a BAS agent and Tax agent and who works directly with professional accountants and business advisors? This is the ideal scenario for a business owner as you can essentially get it all done in one place! And that’s exactly how we’re set up at Numera! Having your bookkeepers and accountants working hand in hand is the best solution for a business owner as you can be sure everyone is working on the same page, seamlessly.

If your business needs support with BAS preparation and lodgement, don’t hesitate to give us a call on 07 3002 4880. The team at Numera are both Registered BAS agents and Registered Tax agents and we have experience with all the major accounting software packages, including Xero BAS, MYOB, Quickbooks and Reckon. With significant experience across a wide range of industry sectors, we are able to support you with all the standard bookkeeping services as well as advising on the most appropriate accounting method for your business.